Health insurance serves as a financial safety net that protects individuals and families from overwhelming medical expenses. This contractual arrangement between policyholders and insurance companies ensures access to quality healthcare services without depleting personal savings. The system operates on the principle of risk distribution, where multiple subscribers contribute premiums to create a pool of funds that covers medical treatments for those who need them.

Medical coverage has become an essential component of financial planning in modern society. The rising costs of hospital bills, prescription medications, and diagnostic procedures make uninsured medical emergencies financially devastating. Statistics demonstrate that medical debt remains one of the leading causes of personal bankruptcy in many countries.

Types of Health Insurance Plans

Individual Health Insurance

Individual health insurance policies provide coverage for single persons who purchase plans directly from insurance providers or through government marketplaces. These policies offer flexibility in choosing coverage levels and premium amounts based on personal health needs and financial capabilities.

Family Floater Plans

Family health insurance extends protection to multiple family members under a single policy. This arrangement typically includes spouses, dependent children, and sometimes parents. The sum insured floats among all covered members, allowing any family member to utilize the entire coverage amount if necessary.

Group Health Insurance

Employers frequently offer group health insurance as part of employee benefit packages. These plans generally provide comprehensive coverage at lower premium rates because the risk spreads across a large group of employees. Group medical insurance often includes additional benefits like dental care, vision coverage, and wellness programs.

Government-Sponsored Programs

Various government initiatives provide affordable healthcare options for eligible populations. These programs target specific demographics including low-income families, elderly citizens, veterans, and children from economically disadvantaged backgrounds.

Essential Components of Health Insurance

Premium Payments

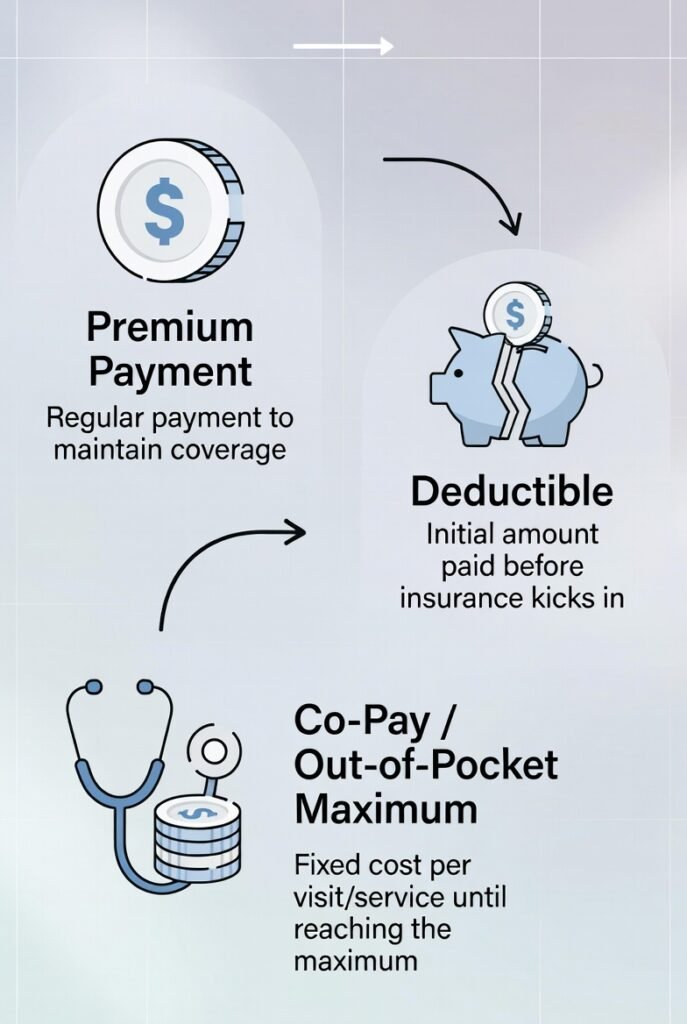

The insurance premium represents the amount policyholders pay regularly to maintain active coverage. Insurance companies calculate premium costs based on multiple factors including age, medical history, lifestyle habits, geographic location, and selected coverage options.

Deductibles and Their Impact

A deductible constitutes the amount policyholders must pay out-of-pocket before insurance coverage activates. High-deductible plans feature lower monthly premiums but require substantial upfront payments during medical events. Conversely, low-deductible options charge higher premiums while reducing immediate financial burden during healthcare utilization.

Co-payments and Co-insurance

Co-payment refers to fixed amounts patients pay for specific services like doctor visits or prescription medications. Co-insurance represents a percentage of medical costs that policyholders share with insurance companies after meeting the deductible. Understanding these cost-sharing mechanisms helps individuals estimate total healthcare expenses.

Out-of-Pocket Maximum

The out-of-pocket maximum establishes a ceiling on annual medical expenses. Once policyholders reach this limit, insurance companies cover 100% of additional covered services for the remainder of the policy year. This provision protects families from catastrophic medical bills.

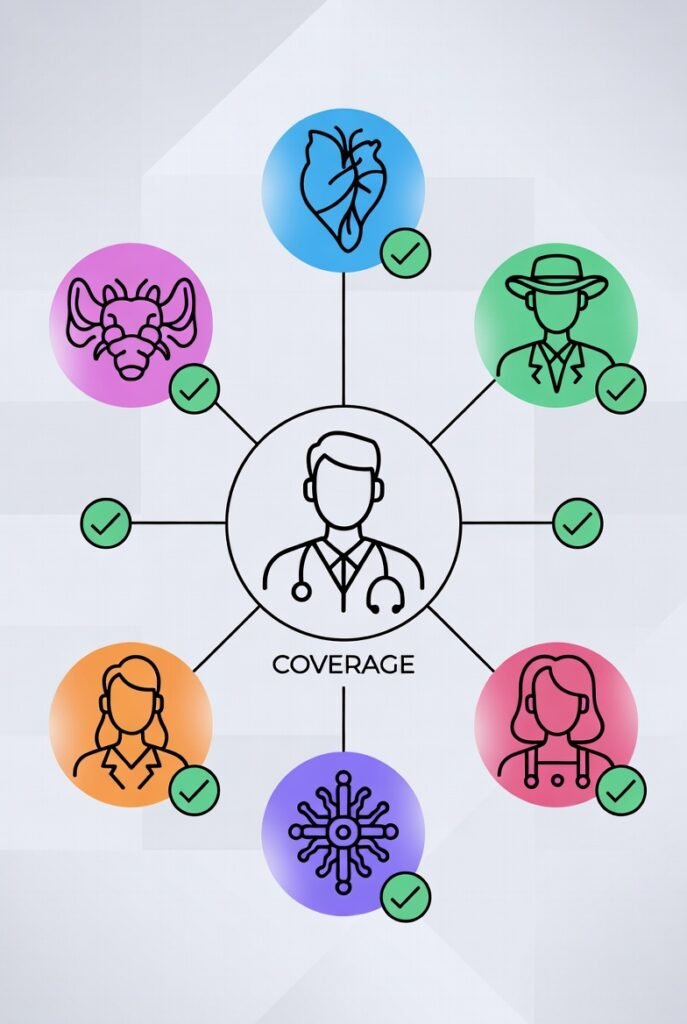

Coverage Benefits and Services

Hospitalization Coverage

Inpatient care coverage includes room charges, surgical procedures, intensive care unit stays, and post-operative recovery. Hospitalization benefits typically cover accommodation expenses, nursing care, surgeon fees, anesthesia costs, and medical supplies used during treatment.

Outpatient Services

Outpatient treatment encompasses medical services that don’t require overnight hospital stays. This category includes diagnostic tests, laboratory work, radiology services, minor surgical procedures, and specialist consultations. Modern health insurance policies increasingly recognize the importance of comprehensive outpatient coverage.

Prescription Drug Coverage

Medication coverage helps manage the costs of prescribed pharmaceuticals. Insurance companies maintain formularies that categorize medications into tiers, with generic drugs receiving the most favorable cost-sharing arrangements and specialty medications requiring higher patient contributions.

Preventive Care Services

Preventive healthcare focuses on early detection and disease prevention. Covered services often include annual physical examinations, immunizations, cancer screenings, cardiovascular assessments, and wellness counseling. Many policies provide preventive services without charging deductibles or co-payments.

Emergency Medical Care

Emergency coverage protects policyholders during urgent medical situations requiring immediate attention. This benefit covers emergency room visits, ambulance services, trauma care, and stabilization treatments regardless of whether patients receive care at in-network or out-of-network facilities.

Network Providers and Access

In-Network vs. Out-of-Network

In-network providers maintain contractual agreements with insurance companies to offer services at pre-negotiated rates. Utilizing network healthcare providers results in lower out-of-pocket expenses. Out-of-network care typically involves higher costs because providers haven’t agreed to discounted fee schedules.

Primary Care Physicians

Many plans require members to select a primary care physician who coordinates all healthcare needs. This doctor serves as the first point of contact for medical concerns and provides referrals to specialists when necessary. This care coordination approach improves treatment outcomes while controlling costs.

Specialist Access

Specialist care addresses specific medical conditions requiring advanced expertise. Some insurance plans allow direct specialist access, while others mandate primary care referrals. Understanding these access requirements prevents unexpected claim denials.

Factors Affecting Insurance Costs

Age and Health Status

Premium calculations heavily weigh age factors, with older individuals typically facing higher costs due to increased health risks. Pre-existing conditions, chronic diseases, and previous medical history influence underwriting decisions and pricing structures.

Geographic Location

Healthcare costs vary significantly across regions based on local medical service prices, state regulations, and competitive market dynamics. Urban areas often feature more provider options but may charge higher premiums than rural regions.

Tobacco Usage and Lifestyle

Insurance companies frequently impose surcharges on tobacco users due to associated health risks. Lifestyle factors including obesity, alcohol consumption, and occupational hazards also impact premium rates.

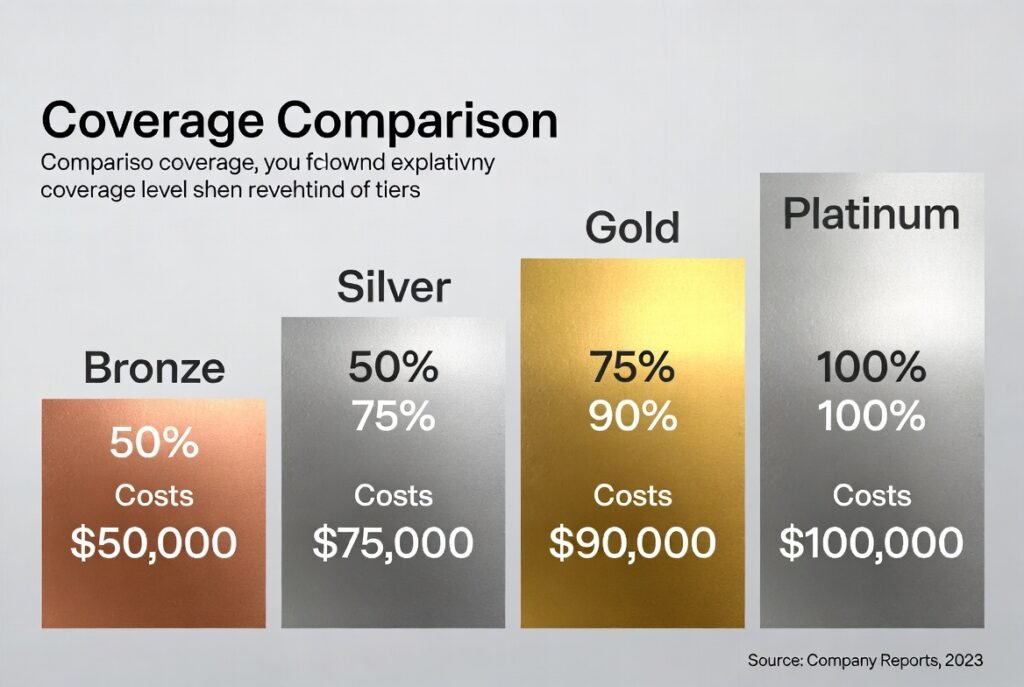

Coverage Level Selection

Plan selection directly influences costs. Bronze-tier plans offer minimal coverage with low premiums, while platinum-level options provide comprehensive benefits at premium prices. Silver and gold plans occupy middle positions, balancing affordability with coverage breadth.

How to Choose the Right Plan

Assess Healthcare Needs

Evaluating anticipated medical requirements guides appropriate plan selection. Families with young children prioritize pediatric care and immunization coverage. Individuals managing chronic conditions seek plans with robust prescription benefits and specialist access.

Compare Total Costs

Smart consumers analyze total annual expenses beyond monthly premiums. Calculating potential deductible payments, expected co-payments, and out-of-pocket maximums provides accurate cost projections.

Review Provider Networks

Verifying that preferred doctors, hospitals, and specialists participate in plan networks prevents disruptions in established care relationships. Network directories help confirm provider participation before enrollment.

Understand Coverage Limitations

Reading policy documents reveals coverage exclusions, waiting periods, and benefit limitations. Understanding these restrictions prevents unpleasant surprises during claim submission.

Claim Process and Reimbursement

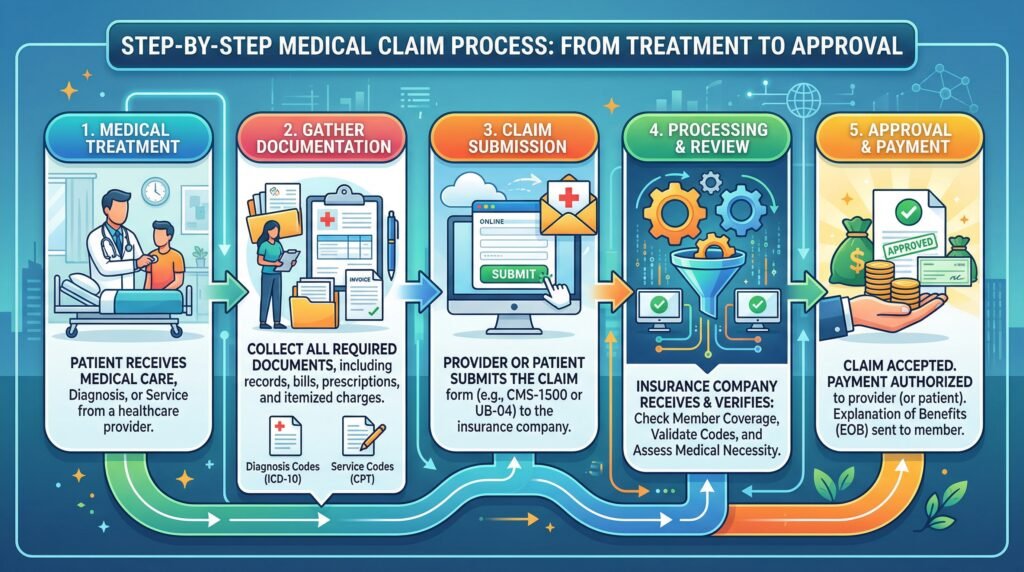

Filing Insurance Claims

The claim submission process involves providing documentation of medical services received. Cashless treatment arrangements allow direct billing between providers and insurers, eliminating upfront payments. Reimbursement claims require policyholders to pay initially and submit receipts for compensation.

Required Documentation

Successful claim processing depends on complete documentation including medical reports, prescription orders, hospital bills, diagnostic test results, and doctor certificates. Maintaining organized medical records expedites reimbursement.

Claim Settlement Timeline

Insurance companies typically process straightforward claims within 7-30 days. Complex cases requiring additional investigation may extend settlement timelines. Understanding these timeframes helps manage expectations.

Common Exclusions and Limitations

Health insurance policies exclude certain treatments and conditions. Cosmetic procedures, experimental therapies, self-inflicted injuries, and pre-existing conditions during waiting periods typically lack coverage. Alternative medicine treatments often fall outside standard policy coverage. Understanding these exclusions prevents claim rejections.

Conclusion

Health insurance represents a critical investment in financial security and wellbeing. Comprehensive coverage protects families from devastating medical expenses while ensuring access to quality healthcare services. Informed plan selection requires careful evaluation of personal needs, cost considerations, and coverage features. As medical costs continue rising, securing appropriate health insurance coverage becomes increasingly essential for maintaining both physical health and financial stability. Taking time to understand policy terms, comparing available options, and selecting appropriate coverage levels empowers individuals to make confident decisions about their healthcare protection.